Industry Information Daily

2021-09-13 11:18

[Abstract]LCD TV panel prices are falling sharply: LCD TV panel prices have been soaring for more than a year, but they began to decline in the third quarter of 2021.

--This article is from Omdia.

LCD TV maker to face sharp drop in panel prices in second half of 2021 after surge in supply chain costs

| Release date: 2021/8/31 Source:Omdia |

| Abstract:

|

LCD TV panel prices are falling sharply: LCD TV panel prices have been soaring for more than a year, but they began to decline in the third quarter of 2021.

2021The panel price dive in the second half of the year was mainly driven by competition among TV manufacturers; the widening difference in interest rates between Chinese TV manufacturers and South Korea TV manufacturers, coupled with the strong bargaining power of the two-Korean TV brand manufacturers in the supply chain, accelerated the decline in LCD TV panel prices. However, the rapid decline in panel prices is not what first-line TV manufacturers are happy to see. How do TV manufacturers take up the risk of plunging TV monitor prices and maintain the competitive landscape changed by the tight supply chain of first-line manufacturers in the past year-good money drives out bad money and the opportunity to increase the value of the TV supply chain-this will test how TV monitor supply chain participants should adjust their operations and competitive strategies, with the increasing difficulty of forecasting the future of supply chains and televisions, it is the common goal and responsibility of all participants to achieve sustainable management.

LCD TV panel prices have been soaring for more than a year; the decline began in the third quarter of 2021, with a large and fast decline

At the beginning of the third quarter of 2021, participants in the TV panel supply chain feel that there is no longer a shortage of LCD panels, and due to global logistics problems and the extremely tight supply of electrical components, TV manufacturers are no longer actively purchasing panels in large quantities, and the bargaining power of the LCD panel supply chain has returned to TV manufacturers.

2021July was a crucial month. LCD TV panel prices reversed, and the panel price negotiations. Panel price negotiations include requiring MDF(market development funds) and price protection for some TV manufacturers. This makes panel manufacturers feel more pressure, because TV manufacturers in the third quarter of the panel demand forecast, but also delayed the fourth quarter of the panel purchase order or said that it may significantly reduce the initial purchase plan. As of mid-August, only a few TV manufacturers have finalized the panel price for July. Most TV manufacturers are reluctant to finalize panel prices for July and August before the end of the third quarter of 2021.

The following is Omdia's observation of LCD TV panel price trends, based on a survey of the TV panel industry supply chain in mid-August. Omdia believes that panel prices will fluctuate greatly in the third and fourth quarters of 2021. History may repeat itself-large price adjustments may follow a panel price surge, especially in the early stages of a panel price decline.

• Panel price negotiations have been rocky since July 2021. The back-and-forth communication between panel manufacturers, TV brands/OEMs and retailers will continue until September 2021, covering panel shipments in the third quarter of 2021.

• Overall TV demand in the end market, including developed markets where TV shipments grew in 2020, has been weakening (compared to the unusually strong consumer demand triggered by the new crown epidemic in 2020). Although this is the reason why the panel demand is not so strong, the main reasons for the upcoming panel price correction that may be larger and faster are the following:

• The profit distribution of the whole TV panel supply chain is unbalanced. When panel manufacturers announce record profits in the second quarter of 2021, this means that the bargaining power of the supply chain may change. Conversely, when panel manufacturers suffer large losses, the signal of a rebound in panel prices will also be evident.

• 2021Panel manufacturers' profit margins soared in the second quarter. South Korea's first-tier brands made better profits in the second quarter of 2021, but China's TV makers continued to decline in profit margins.

• 2021In 2010, larger TV manufacturers developed more powerful. When TV manufacturers are urged to accelerate the migration to feature-rich large-size TVs, it is possible to restore a healthy or profitable TV panel business environment. However, in this unprecedented supply shortage, low-end TV machine manufacturers face a major risk of being squeezed.

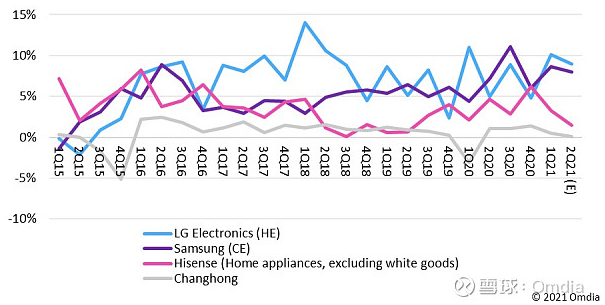

• Compared with the performance in the first quarter of 2021, despite the continuous increase in panel prices in the first half of 2021 and other supply chain problems, such as logistics problems and shortage of non-panel TV materials, South Korea first-line brands Samsung and LG Electronics were able to maintain their TV business operating profit margins in the second quarter of 2021 at a level similar to that in the first quarter of 2021. South Korea brands' profit margins are better than their industry peers due to their strong push to large/oversized migration with advanced TV features, competitive supply chain management of panel pricing and logistics arrangements, and strong brand negotiation ability to bargain with retailers to increase TV average selling prices. Entering the second half of 2021, Samsung and LG Electronics are expected to achieve higher profit margins in the third quarter of 2021, but Chinese TV manufacturers will face greater challenges, as shown in Figure 1. This will prompt Chinese TV manufacturers to more actively require panel manufacturers to provide lower panel prices.

Figure 1: Quarterly Operating Margin of TV Machine Manufacturers (%)

• The shortage of non-panel parts, especially electrical parts, has caused TV manufacturers to no longer rush to actively purchase panels in the second half of 2021, because even if they prepare the panels, no parts will be shipped.

• Logistics problems-container shortages, container ship jams and soaring transportation costs-have made TV manufacturers and retailers very anxious, which has damaged their supply chain arrangements and profit management to cope with the upcoming, very critical fourth quarter promotion season. Coupled with the supply of electrical accessories and global logistics issues, the production plans of TV manufacturers in the second half of 2021 are being affected.

• TV manufacturers and retailers must pay extremely high prices to ship goods from Asia to North American or European markets. Some people are worried about the upcoming promotion season, because if it cannot reach the end market in time for the holiday promotion season, some goods will end up as hidden inventory, which is risky.

• OmdiaThe sharp and rapid decline in panel prices is expected to begin in the middle of the third quarter of 2021. This allows TV manufacturers to purchase panels more conservatively before the end of the panel price adjustment. As analyzed by Omdia in the TV Panel and OEM Information Services report, Omdia believes that TV manufacturers will reduce their panel purchase forecasts for the third and fourth quarters of 2021.

• 2021In the third quarter of the year, TV panel prices showed a downward trend, so some TV manufacturers are eager to clean up their TV goods and inventory and sell them at a lower price in the market to avoid more inventory losses, because these TVs are equipped with high-priced panels. Before panel makers agreed to offer panel price concessions to TV makers, some TV makers were forced to cut their average TV prices further because they found it difficult to boost TV sales-especially in the Chinese market-despite some price cuts in July 2021. This means that TV manufacturers will have to do more promotional activities to drive sales. TV manufacturers will continue to require panel manufacturers to provide more concessions by providing MDF, reducing panel prices and price protection. Alternatively, they will make more cuts in panel purchases in the third and fourth quarters of 2021.

• Whenever there is a clear signal of a downward trend in panel prices, the display panel supply chain participants will fall into a vicious circle. TV makers and retailers are trying to predict how far panel prices will fall in the current downward cycle. TV manufacturers cannot predict whether the recent surge in panel prices is likely to fall to the lowest price level in history in November 2019 or the low price level in May 2020 of the previous cycle. There are several dynamic changes in the supply base of LCD panels. At present, the most obvious change is the decrease in the number of LCD panel suppliers, and the dominance of Chinese panel manufacturers in panel shipments, product size/function and production capacity.

• TV makers are actively negotiating with panel makers to make big price concessions to compensate for promotions and boost sales, especially in China. TV manufacturers are also pushing panel manufacturers to reduce the average price of panels to improve their financial situation to a certain extent. However, TV manufacturers are also worried about the loss of inventory prices, and the decline in TV panel prices will scare away demand from retailers.

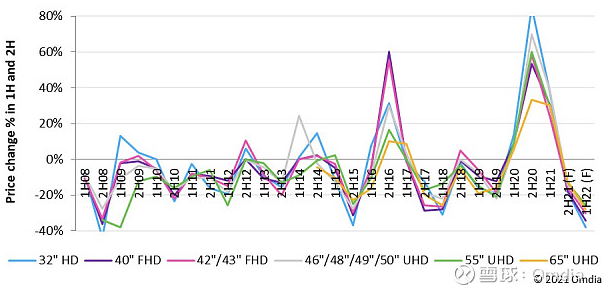

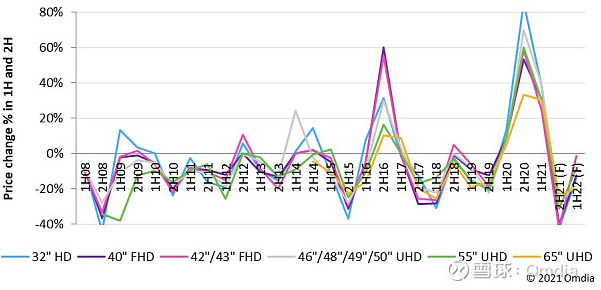

• OmdiaThe panel price trend is expected to decline sharply in 2022, as shown in Figure 2. However, based on the results of a recent supply chain survey conducted in mid-August 2021 on TV maker target panel prices for the third and fourth quarters of 2021, Omdia has begun to notice a sharp change in panel price trends (as shown in Figure 3). This suggests that the panel price correction originally expected in the first half of 2022 has been advanced to some extent to the second half of 2021.

Figure 2: Panel price changes in the first half and second half of 2008-2022, updated July 2021

Figure 3: Panel price changes in the first half and second half of 2008-2022, updated in August 2021 (based on the target price of TV manufacturers in the second week of August 2021)

Chart Description:

1. Price changes in the first half of the historical year are based on price changes between June and December (for example, the data for the first half of 2008 is a price comparison between June 2008 and December 2007).

2. The price changes in the second half of the historical year are based on the price changes between June and December (for example, the data for the second half of 2008 is the price comparison between December 2008 and June 2008).

3. 2012Before, panel prices were based on CCFL(module cold cathode fluorescent lamps). Starting from January 2012, panel prices are based on open cell.

4. From April 2014, the 50-inch UHD became the dominant size in the mid-range size category.

5. Starting in May 2008, the price of 55 inches became available.

6. Starting from April 2014, the price of 65 inches will be available.

More Latest Developments

Strengthening the Chain and Laying the Foundation for a New Journey: Grand Commissioning Ceremony of Qingyi Optoelectronics' Foshan Nanhai Production Base

2025-11-27

DIC EXPO 2025: Qingyi Optoelectronics Shines on the International Display Technology Stage

2025-08-15

Service Hotline:

Fax: 86-755-86352266

E-mail:sales@supermask.com

Address: Beiqingyi Opto-electronic Building, Langshan 2nd Road, Nanshan District, Shenzhen City

Copyright © 2025 Shenzhen Qingyi Photomask Limited All rights reserved.

{kind=link}